+91 9828123489

+91 9828123489 +91 9828123489

+91 9828123489 help@vakilkaro.co.in

help@vakilkaro.co.in

The Income Tax Department provides relief to taxpayers when they incur any losses. The relief is provided as a deduction from the Taxpayer’s Income with some conditions and restrictions. This is the opposite side of the Income Tax Department which is known for the collection of huge taxes on Taxpayer’s Income.

Set off means setting off the loss in the same Assessment Year in which it is incurred.

Carrying forward and set off means carrying forward the losses and setting them in the future years.

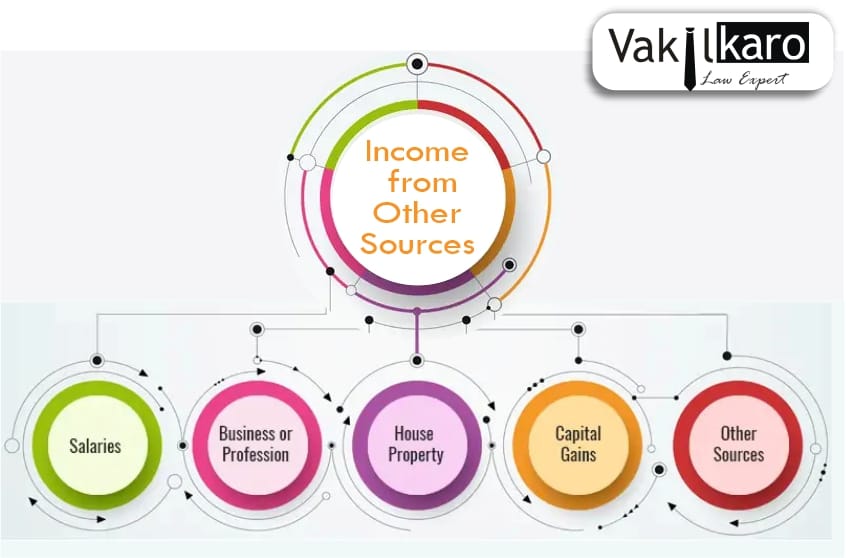

There are a total of five heads of income under the Income Tax Act namely:

i. Salary Income

ii. Profit or Gains from Business or Profession

iii. Capital Gains Income

iv. House Property Income

v. Other Sources Income

The Taxpayers income is divided into the above five categories for the collection of taxes.

There can never be a loss under the head salary. Hence there is no provision for Set-off and carry forward of its losses. The losses incurred under the head Other Sources are not allowed to be carried forward and set off.

Set-Off

There are two ways in which Set off of the losses is possible:

i. Intra Head Adjustment

ii. Inter Head Adjustment

Intra Head means setting off the loss within the same head. Example: Setting off the loss under PGBP from export business with the income under PGBP from manufacturing business. The Income Tax Act allows each kind of Intra adjustments except the following:

i. Loss incurred from speculative business cannot be set off against non-speculative business income. For Example, Loss incurred from the Intra-day transactions of shares cannot be set off against the loss from the manufacturing business. But Losses from non-speculative businesses can be set off with income from speculative business.

ii. Long Term Capital Loss cannot be set off with Short Term Capital Gain.

iii. Loss from casual income cannot be set off against any income. Casual income includes Income from lotteries, crossword puzzles, gambling or betting, etc.

iv. Losses from the business of owning and maintaining race horses cannot be set off against any income except income from the same business.

v. Losses from the business specified under Section 35AD (Specified Business) cannot be set off against Incomes except income from the same business. But Losses from Non-Specified Businesses can be set off against the Income of Specified businesses.

Inter Head means setting off the loss of one head with the income of the other head. Example: Setting off House Property Loss with the Salary Income. Under the Income-tax Act all kinds of Inter head adjustments are allowed except the following cases:

i. Losses from speculative business cannot be set off against income under any other head.

ii. Losses under the head PGBP cannot be set off against Salary Income.

iii. Losses under the head Capital Gain cannot be set off against any other head. But Losses under any other head can be set off with Income under the head Capital Gain.

iv. No loss can be set off against casual incomes.

v. Losses from the business of owning and maintaining race horses cannot be set off against any other head.

vi. Loss from the business specified under section 35AD cannot be set off against any other head of income.

Carry Forward and Set-off

The losses which could not be set off either by way of Intra head adjustments or Inter head adjustments are allowed to be carried forward to the future years subject to the conditions and restrictions as prescribed by the Act. Income Tax Act does not allow Carry forward and set off of Losses under the head Other Sources.

Losses under the various heads of income can be carried forward and set off only if the return has been filed on or before the due date of filing the return of income. But this provision does not apply in case of carrying forward of Loss under the head Income from House Property, it means loss under the head house property can be carried forward even if the return is filed after the due date.

However, there is no restriction on setting off the losses if the return is filed after the due date.

Losses under the head PGBP: It can be set off against any income except salary in the year the loss is incurred. If the loss could not be set off in the year loss was incurred it can be carried forward up to 8 Assessment Years and loss will be allowed to be set off against income under the head PGBP. It can be simply concluded that in the year the loss is incurred both Intra & inter head adjustments are possible, but in the years of carrying forward only intra head adjustments are possible.

Losses under the head Capital Gains: It can be set off or carried forward and set off in the following manner:

Losses Set off/Carry forward and Set-off

Long Term Capital Loss Long Term Capital Gain

Short Term Capital Loss Long Term Capital Gain/Short Term Capital Gain

.png)

.png)

.png)

.png)

.png)

.png)

+91 9828123489

+91 9828123489 help@vakilkaro.co.in

help@vakilkaro.co.in